Content

Receipts from the sale for such items as scrap or recoveries of building costs for such items as change orders and insurance should be deducted from the amount of the project to be capitalized. Land is carried on the Reserve Bank’s books at cost and is not depreciated. These accounts consist of the four accounts listed in the Bank Premises section of the FR 34 balance sheet, the Furniture and Equipment account and its related allowance for depreciation account, and the Other Real Estate account listed in the Other Assets section of the FR 34. This chapter also gives instructions concerning leasehold improvements and software which are discussed in Deferred Charges (see also paragraph 4.20). It is also used in financial statements such as the balance sheet to indicate the depreciation worth of assets over time.

- If the real estate contains a building that will eventually be razed, depreciation should be discontinued upon acquisition.

- Payments for penalties for terminating the lease if the lease term reflects the lessee exercising an option to terminate the lease.

- Accounting PrinciplesAccounting principles are the set guidelines and rules issued by accounting standards like GAAP and IFRS for the companies to follow while recording and presenting the financial information in the books of accounts.

- Replacements should be accounted for under the substitution approach which requires removing the cost of the existing asset and its accumulated depreciation from the books and charging current expense for the difference.

- In that case, you will debit the depreciation expense and credit the accumulated depreciation for the same amount to reflect the asset’s net book value on the balance sheet.

Any transfer of assets between offices of the same District should be made at book value. The receiving office should record the asset on a cost basis equal to the net book value. Disposals are not necessarily write-downs or impairments, which must be approved by the RBOPS Accounting Policy and Operations Section.

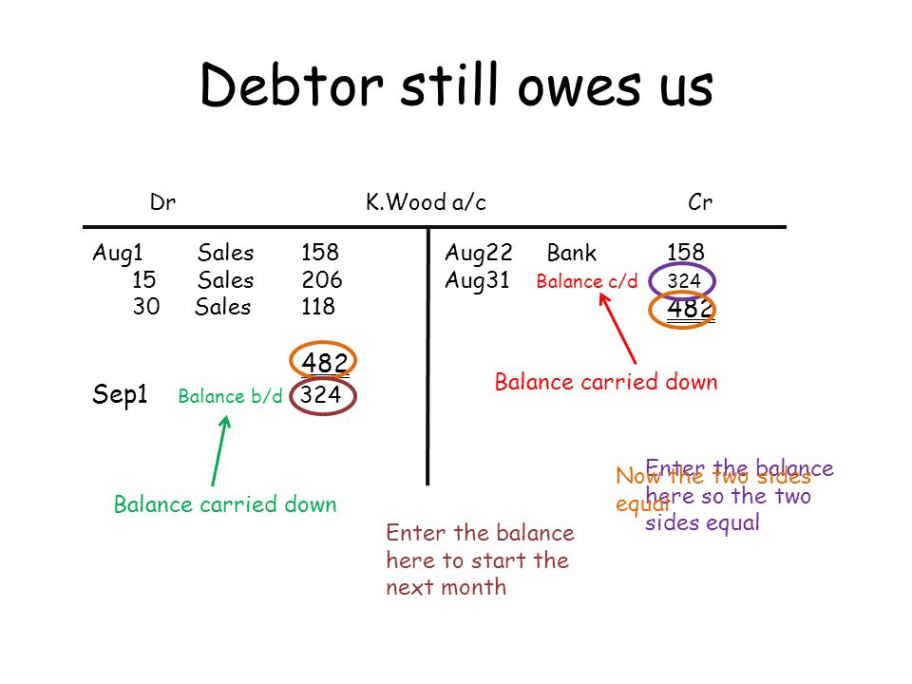

Debit or Credit?

However, when you eventually sell or retire an asset, you debit the accumulated depreciation account to remove the entry for that asset. The IRS requires businesses what is accumulated depreciation equipment to depreciate specific assets using the Modified Accelerated Cost Recovery System . For this method, the IRS assigns a useful life to various asset types.

Are accumulated depreciation equipment an asset?

Accumulated depreciation is not an asset because balances stored in the account are not something that will produce economic value to the business over multiple reporting periods. Accumulated depreciation actually represents the amount of economic value that has been consumed in the past.

Although it is reported on the balance sheet under the asset section, accumulated depreciation reduces the total value of assets recognized on the financial statement since assets are natural debit accounts. In accounting, an asset is depreciated to recognize the decline in value over its service life and production activity. Depreciation expense is calculated using various methods, such as the straight-line or declining balance method. While depreciation expense refers to the depreciation incurred on the asset in the present year, an asset’s accumulated depreciation represents the total, cumulative depreciation on the asset since it has been placed in service. If the new item will not be pooled, it should be expensed at the net purchase price; lost, stolen or junked, with no salvage or trade-in value received, no entries are to be made for Balance Sheet accounting and reporting purposes.

IAS 16 — Proceeds before intended use

It is the total amount of an asset that is expensed on the income statement over its useful life. Prior to 2021, the pooled asset method was used to account for furniture, furnishings, and fixtures. Pooling allowed small dollar/large quantity assets to be appropriately reflected on the financial statements without imposing the unnecessary tracking of each asset individually as a practical expedient. Under the pooled asset accounting concept, no individual item had a recorded and separately identifiable book value.

- As a contra-asset account, accumulated depreciation has a normal credit balance.

- Depreciation is the process of allocating the cost of equipment over its useful life, and accumulated depreciation reflects the total depreciation recorded for that equipment over time.

- Accumulated depreciation is the sum of current and prior periods’ depreciation expenses.

- Each year the contra asset account referred to as accumulated depreciation increases by $10,000.

For custom built or constructed equipment or facilities, depreciation calculation begins one month after the item is put into service. When an item is disposed of, depreciation is taken through the month of disposal. Since the salvage value is assumed to be zero, the depreciation expense is evenly split across the ten-year useful life (i.e. “spread” across the useful life assumption).

Is Accumulated Depreciation equipment an expense?

Depreciation expense is the amount that a company's assets are depreciated for a single period (e.g, quarter or the year), while accumulated depreciation is the total amount of wear to date. Depreciation expense is not an asset and accumulated depreciation is not an expense.